When you hire a rental car, the agreement usually includes insurance, but it also comes with an excess. This is the amount you must pay if the vehicle is damaged or stolen during your rental period.

The problem is that 58% of damage claims aren’t caused by the renter at all. A stone chip from another vehicle, a car park ding while you’re inside shopping, or vandalism overnight can still leave you responsible for the excess.

These charges aren’t small either. Some rental companies set excess limits as high as $6,900 for standard vehicles, and plenty sit around the $5,000 mark. That’s a serious chunk of money to lose over a cracked windscreen or a scratched bumper you didn’t cause.

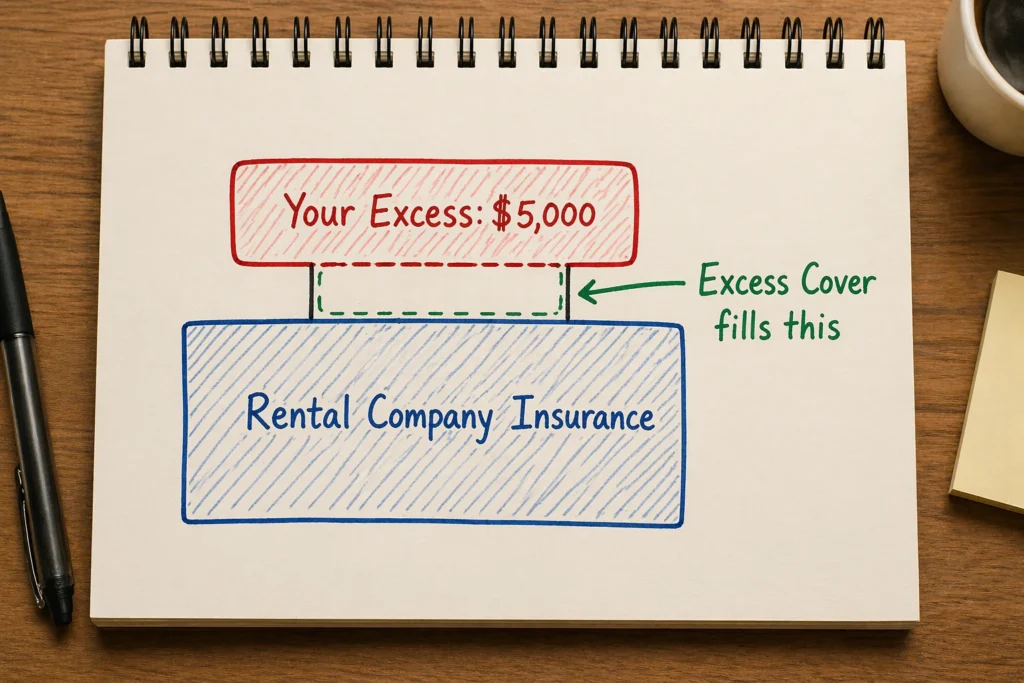

Car hire excess insurance covers this risk. It works alongside the rental company’s own insurance rather than replacing it.

What Is Car Hire Excess Insurance?

Car hire excess insurance is a policy that reimburses you for the excess the rental company charges if their vehicle gets damaged or stolen. When you pick up a rental vehicle, the car rental company provides basic rental car insurance covering major damage, theft, and third-party liability.

That insurance comes with an excess amount, which is what you pay out of your own pocket before the insurer covers the rest.

On average, excess charges are around US$1,169. The rental company’s insurance handles the larger claim, but you’re still liable for that excess portion upfront.

Excess cover fills this gap. It doesn’t replace the rental agreement’s insurance. Instead, it protects you from paying over a thousand dollars (sometimes much more) when the rental vehicle gets a scrape or a cracked windscreen.

How Car Hire Excess Insurance Works

Car hire excess insurance works in two stages: you purchase cover before collecting your rental, then claim back the excess if damage occurs. Unlike the rental company’s counter insurance, you pay the depot’s excess charge first and get reimbursed afterwards.

The Reimbursement Process

Excess insurance is typically purchased before you collect your rental vehicle, either as single-trip cover for one hire or annual cover if you rent cars multiple times a year.

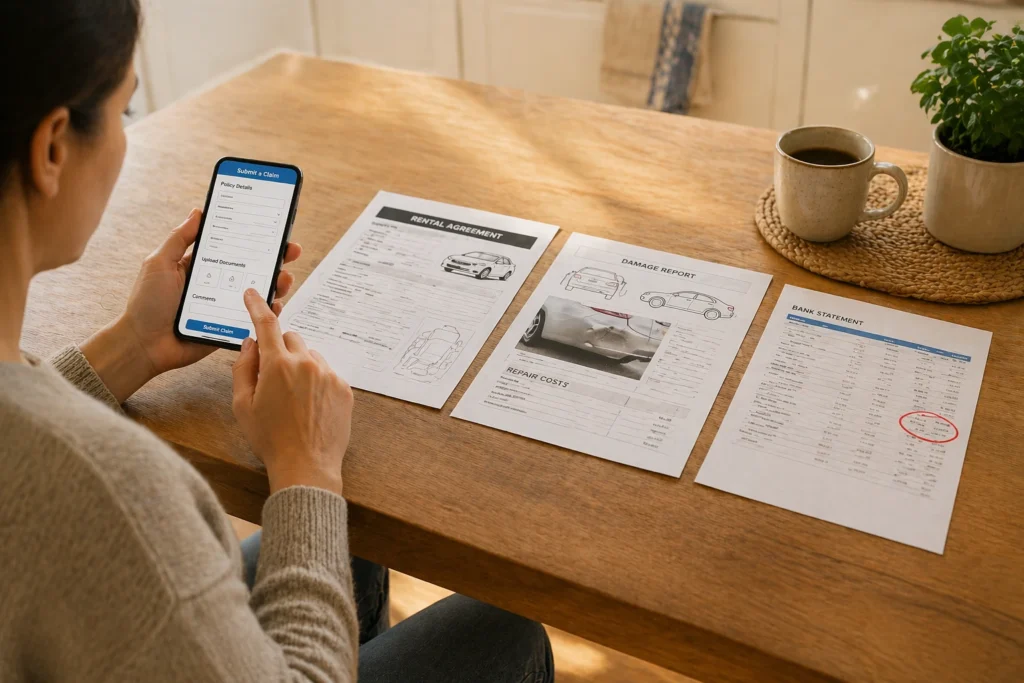

If damage occurs, the rental company charges the rental car excess to your credit card as outlined in your rental vehicle agreement. You then file a claim with your excess insurance provider, submitting receipts and the damage report to recover the amount.

Making a Claim on Your Excess Cover

The claim process usually starts after the rental company has charged you for the damage or loss. Most insurers require you to submit your claim within 31 days of the car hire excess charge appearing on your statement. You’ll typically need your rental agreement, a damage report showing repair costs, and proof of payment.

Once submitted, most insurers process claims within around two weeks and refund the amount directly to the card you used for the purchase.

What’s Covered and What Isn’t

Excess insurance policies vary widely in what they cover. Some include extras like tyres and windscreens, while others stick to basic bodywork damage. Most standalone policies typically cover the following, while common exclusions still apply:

- Damage to the Vehicle Body: This is the bread and butter of rental vehicle excess cover. It covers scratches, dents, and bodywork damage from accidents or car park scrapes.

- Windscreens and Glass: Cracked windscreens, side mirrors, and headlights typically fall under excess cover, though some policies exclude them entirely (check the fine print before you buy).

- Tyres and Wheels: Most standalone policies cover punctures, blowouts, and wheel damage. The rental company’s insurance often excludes these, which is where your excess cover steps in.

- Theft and Vandalism: If the rental vehicle is stolen or vandalised, you’re covered for the excess the rental company charges. You won’t need to pay the full excess amount yourself, as it can be reclaimed through your policy.

- Single Vehicle Accidents: Most policies cover the excess if you hit a pole, a kerb, or roll the car without another vehicle involved. This includes damage caused in situations where no third party is involved.

- Lost or Stolen Keys: Replacement costs can run into hundreds of dollars. Many excess policies reimburse you for this, though exclusions apply depending on the insurer.

- Misfuelling: Putting petrol in a diesel car (or vice versa) can happen to anyone. Some policies cover the tank drainage and cleaning costs, but not all of them do.

One thing to note: Not all situations are covered. Most policies exclude things like off-road driving, driving under the influence, and interior damage, such as torn seats or stained upholstery. If you breach the rental agreement, excess insurance won’t apply. Coverage also varies between providers, so check the specific policy details before assuming full protection.

Buying Excess Cover: Rental Depot vs Standalone Policy

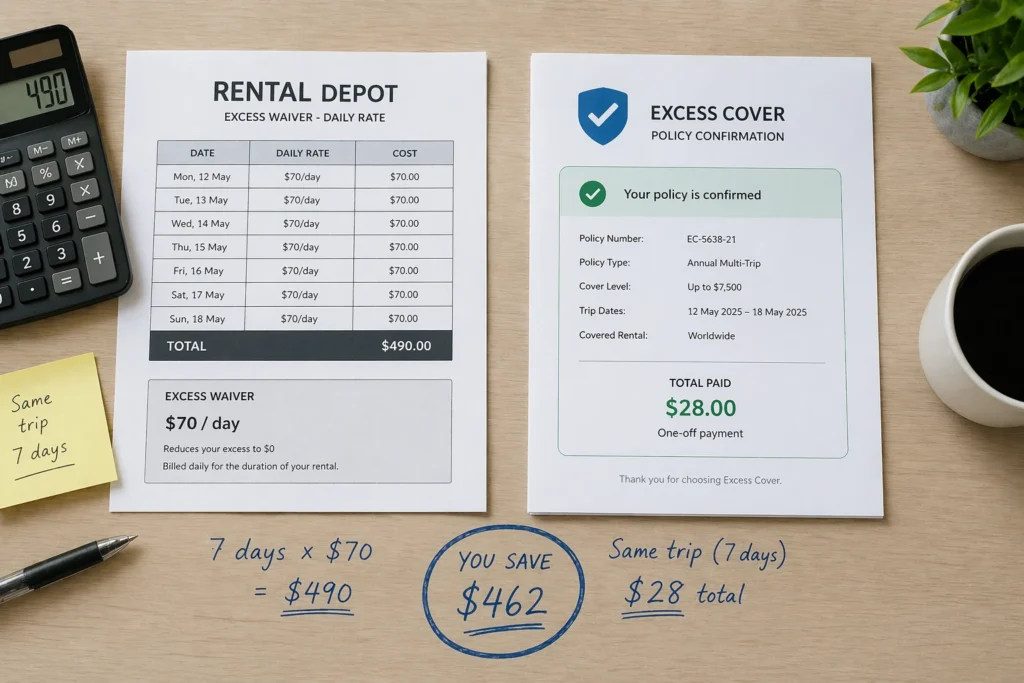

Rental companies offer their own excess waiver at the counter, often called Collision Damage Waiver or excess reduction cover. These waivers can be expensive. For example, some providers charge around $70 per day to reduce your excess to zero, which can nearly double the total rental cost over a week-long hire.

Standalone rental car excess insurance policies bought in advance cost far less. You can find single-trip cover for around $20–30 total, or annual policies for $100–150 that cover unlimited rentals for a year. If you hire cars regularly, the savings from an annual policy add up quickly.

The main trade-off is convenience. Buying cover at the rental depot means you won’t pay anything upfront if damage occurs. Standalone policies, by contrast, require you to pay the rental excess first, then claim it back later. If you don’t mind waiting a couple of weeks for reimbursement, the standalone option saves you hundreds.

Who Should Consider Car Rental Excess Cover?

Anyone hiring a car may want to consider excess cover, but it becomes especially important in certain situations:

- Driving in Unfamiliar Areas: Tight car parks, unfamiliar road layouts, and navigating busy areas like Brisbane’s Fortitude Valley all increase the risk of minor scrapes. Rental car excess cover means a scraped bumper doesn’t cost you over a thousand dollars out of your own pocket.

- High-Value or Specialised Vehicles: When hiring luxury cars or four-wheel drives, excess amounts can reach $8,000–$10,000. That makes excess cover especially worthwhile compared to standard vehicles.

- Frequent Renters: Hiring cars more than once or twice a year makes an annual policy the smarter choice financially. A single claim can often cost more than the annual premium itself.

- Travelling Overseas: Many international travel insurance policies cap rental vehicle excess cover at around $5,000–$6,000, depending on the provider. Standalone excess insurance can help cover higher excess amounts when renting premium or specialised vehicles overseas.

The cost of excess cover is small compared to the potential charges you’d face without it. So check what your existing travel insurance already includes, then decide whether additional protection makes sense for your rental situation.

Where Your Excess Waiver Works

Most standalone excess insurance policies cover rentals across multiple countries, including Australia, Europe, the USA, and Canada. Some insurers limit coverage to specific regions, so it’s important to check your policy matches your destination before booking.

The type of vehicle you hire also affects your cover. Standard policies often exclude off-road use, motorhomes, and certain high-value luxury cars. Four-wheel drives used for city driving are usually covered, but taking the same vehicle onto unsealed roads or beaches may fall outside your protection.

Get the Right Excess Cover Before You Pick Up the Keys

Car hire excess insurance protects you from unexpected charges that can reach into the thousands after minor rental damage. Buying standalone cover in advance usually costs far less than paying for a rental company waiver at the counter.

Before you book car rental excess cover, compare policies, check what’s included, and confirm your rental destinations are covered. If you already have travel insurance, review whether it includes rental vehicle excess cover before adding extra protection.

If you’re ready to plan your trip, get in touch with GLAPacked to choose the right vehicle for your journey.

Related Posts

Is Car Hire Uluru the Right Choice for Your Trip?

Car hire is a great choice for most Uluru trips,…

Car Hire Hobart Airport: How Airport Pickup Works

Car hire at Hobart Airport works much like car hire…

Car Hire Launceston: A Complete Guide for First-Time Renters

Renting a car in Launceston opens up Tasmania in ways…